MARKET REFERENCE · JUNE 2026 · DATA REPORT

UK Broadband Market Share 2026: Who Holds the Market

Who really runs UK broadband: the retail brands you pay, the networks that own the cables, and the altnet challengers reshaping the market. Every figure sourced and dated, including where the official data ends and the best estimates begin.

Written by Dr Alex J. Martin-Smith · Reviewed by Adrian James · Published 11 June 2026 · Refreshed on results seasons and Ofcom data updates · ~9 minute read

Prefer to read offline? Download the free PDF report: UK Broadband Market Share 2026 (6 pages, ~290KB). No signup, no email, just the report.

The quick answer

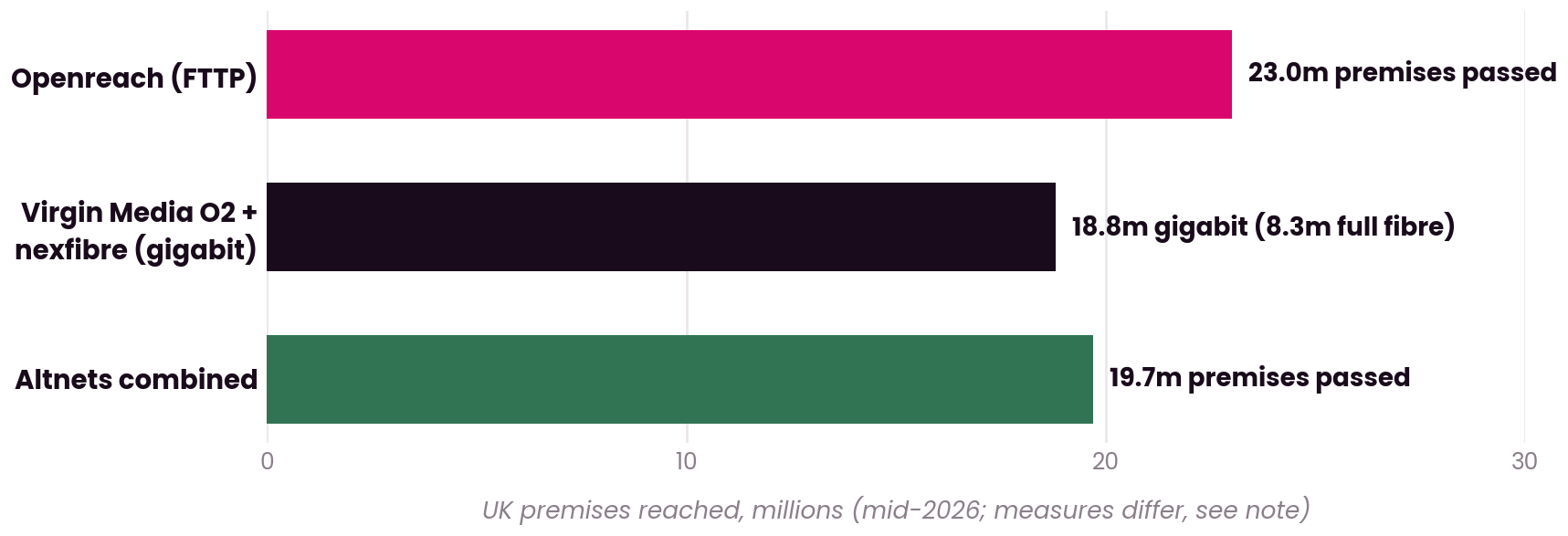

Four groups still dominate the brands UK households pay: BT Group, Sky, Virgin Media O2 and TalkTalk, together about 82% of retail connections on Ofcom's last full published split (2023). Behind them sit three network layers: Openreach (23m FTTP premises, resold by 650+ providers), Virgin Media O2 (18.8m gigabit) and around 80 altnets covering 19.7m premises, with roughly 850,000 customers switching to an altnet between late 2024 and late 2025.

Key facts · verified June 2026

- The UK has 29.3 million fixed broadband lines (Ofcom, Q4 2025).

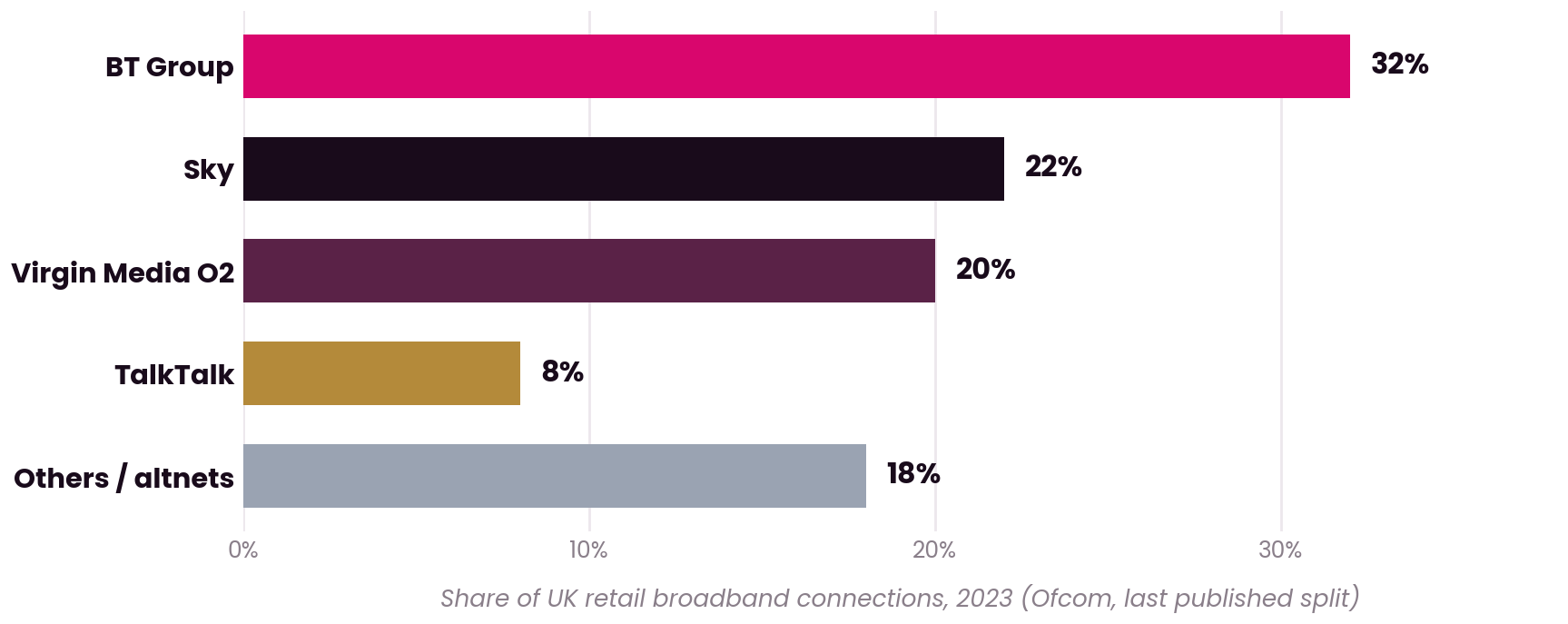

- The big four held ~82% of retail connections on Ofcom's last full split (2023: BT Group 32%, Sky 22%, Virgin Media O2 20%, TalkTalk 8%); no full official split has been published since.

- Current customer bases (best proxies): BT Group ~8.8m (Point Topic, Q3 2025), Sky ~6.7m, Virgin Media O2 5.69m (Q4 2025 results), TalkTalk contracting.

- The network layer: Openreach 23.0m FTTP premises (38% take-up, 25m target by December 2026), Virgin Media O2 18.8m gigabit (8.3m now full fibre), altnets 19.7m combined (INCA), overlapping and not additive.

- Consolidation is under way: nexfibre agreed a £2bn acquisition of Netomnia in February 2026, with the CMA's invitation to comment closed 8 May 2026 and completion expected later in 2026 subject to clearance.

Who you pay: the retail market

That split dates from 2023, because Ofcom's later quarterly data itemises only BT's share, and the picture has shifted since as altnets and Vodafone gain ground. Exact 2026 shares are no longer published, but company results give the latest customer bases. These are the best current proxy.

| Group | Broadband customers | Source |

|---|---|---|

| BT Group (BT, EE, Plusnet) | ~8.8m | Point Topic estimate, Q3 2025 |

| Sky (plus NOW) | ~6.7m | Commercial estimate, UK and Ireland |

| Virgin Media O2 | 5.69m | VMO2 results, Q4 2025 |

| TalkTalk | Contracting | ~120k losses in Q3 2025 (Point Topic) |

Within BT Group, EE is now the lead consumer brand with BT and Plusnet alongside it, and all three resell the Openreach network. Sky and Vodafone also resell Openreach, while Vodafone has been the strongest-growing major brand. Brand-by-brand strengths and head-to-heads live in our provider comparisons.

Who owns the cables: the network layer

Behind those retail brands sit three network layers. Most brands rent space on Openreach; Virgin Media O2 runs its own cable and fibre; and a growing field of altnets has built a third national layer. This is where the real competition now happens, and the full brand-to-network map is in our companion guide: who owns the fibre? The UK wholesale network matrix.

| Network | Reach | Detail |

|---|---|---|

| Openreach (BT Group) | 23.0m FTTP | Take-up 38%; 25m target by Dec 2026; 650+ providers resell it |

| Virgin Media O2 | 18.8m gigabit | 8.3m now full fibre, including the nexfibre joint venture |

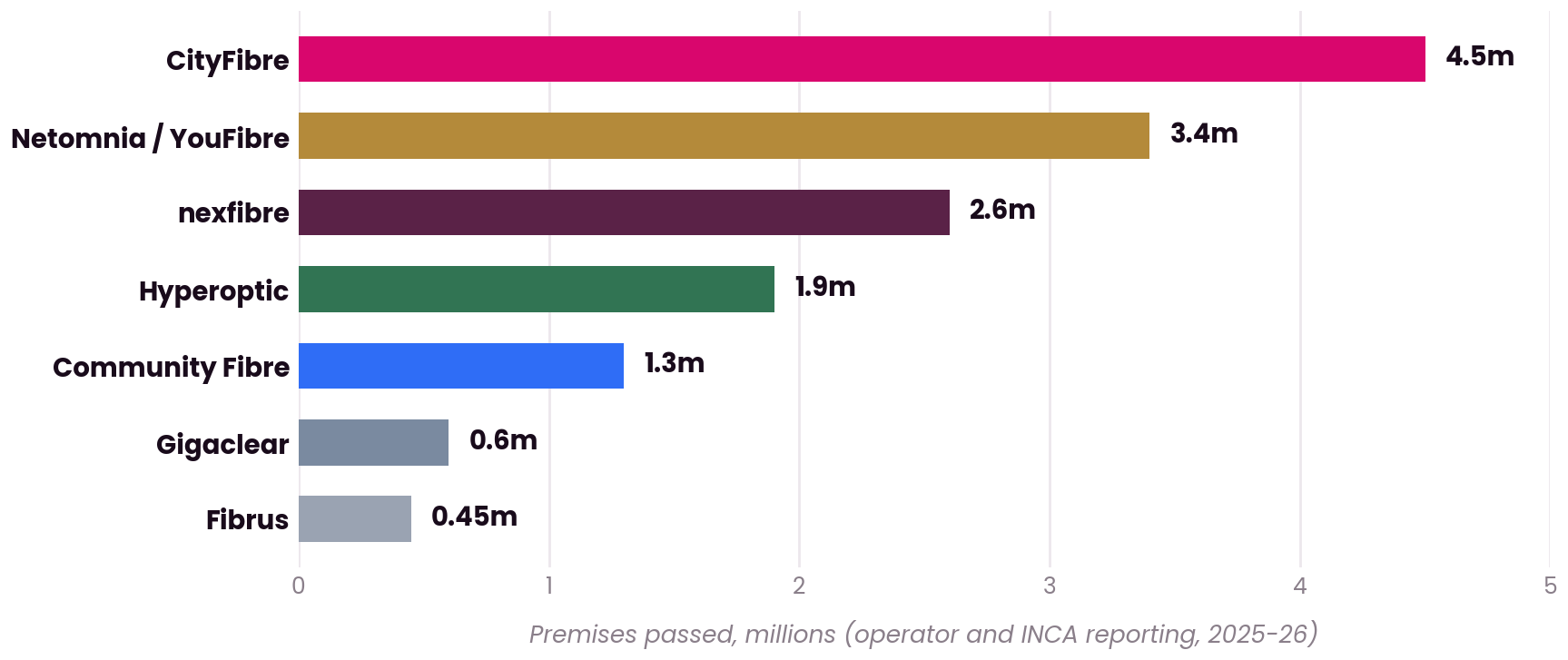

| Altnets combined | 19.7m | 3.5m live connections; an estimated 5m-plus altnet-only |

Openreach is an independently governed, regulated BT subsidiary; most retail brands resell it. Virgin Media O2 is the main vertically integrated alternative, owning its network end to end. Figures: BT Group FY26 results; VMO2 Q4 2025; INCA State of the Altnets 2026.

Why it matters to you: where two or three networks overlap on your street, retail prices fall and choice rises. The network sets your real speed ceiling, so knowing who reaches your address matters as much as the brand on the bill.

Altnets and consolidation

Around 80 alternative networks are tracked across the UK, and between late 2024 and late 2025 roughly 850,000 customers switched to an altnet. Now the field is starting to consolidate.

The deal everyone is watching: in February 2026, nexfibre agreed a £2bn acquisition of Netomnia (owner of YouFibre and Brsk), which would create a wholesale challenger of real scale. The retail brands YouFibre and Brsk would move to Virgin Media O2.

- Where it stands: the Competition and Markets Authority opened an invitation to comment that closed on 8 May 2026. A formal investigation had not yet begun, and completion is expected later in 2026 subject to clearance.

- Why it is contested: CityFibre, the largest altnet, urged the regulator to scrutinise the deal, claiming roughly 80% network overlap and a risk of reduced competition. nexfibre disputes this, pointing to research it commissioned that put the full-fibre overlap nearer 17%. Ofcom has also asked the CMA to take a close look.

- The wider trend: CityFibre has already absorbed Lit Fibre and Connexin, and with build costs high, more consolidation is widely expected.

What the shake-up means for you

A more contested market is good news for households and small businesses. More networks competing on your street tends to mean lower prices and more choice, and switching between them has never been easier.

- Prices are falling in real terms. Ofcom found average broadband prices fell about 6% in real terms in the year to September 2025, with the biggest falls on faster tiers, charted in full in our UK broadband price index 2026.

- Switching is simple. More than two million homes have used One Touch Switch since September 2024, and the loyalty penalty for staying out of contract is £7 to £9 a month.

- Altnets can undercut the big brands. Where an altnet reaches you, entry full fibre often starts well below the national average bill, so it pays to check beyond the household names.

- For SMEs, resilience is the lever. A second network in your area is not just cheaper, it is a genuine backup option if your main line goes down.

The mobile market, for context

Mobile increasingly overlaps with home broadband through bundles and 5G home broadband. The UK now has three mobile network operators.

| Operator | Note |

|---|---|

| EE (BT Group) | Historically the largest mobile network |

| Virgin Media O2 | O2 around 22m subscribers, late 2025 |

| VodafoneThree | Merged 31 May 2025; about 27m customers |

Smaller brands ride these same three networks rather than competing with them. Some are independent (Tesco Mobile, Sky Mobile), while others are owned by the operators themselves, for example Smarty by VodafoneThree and Giffgaff by Virgin Media O2. Together these brands are estimated to account for roughly 17% of the market. The wider statistical backdrop, coverage, speeds and switching, lives in the companion reference: UK broadband statistics 2026.

The technology underneath all three layers is explained in plain English in what is FTTP? Full fibre explained.

Questions people ask

Who is the biggest broadband provider in the UK?

BT Group, with roughly 8.8 million broadband customers across BT, EE and Plusnet (Point Topic estimate, Q3 2025), and 32% of retail connections on Ofcom's last full published split (2023). Sky is second with around 6.7 million, then Virgin Media O2 with 5.69 million.

What market share does each broadband provider have?

On Ofcom's last full published split (2023): BT Group 32%, Sky 22%, Virgin Media O2 20%, TalkTalk 8%, with the remaining 18% across smaller brands and altnets. No full official split has been published since, so current company results and Point Topic estimates are the best proxies.

How many broadband providers are there in the UK?

More than 650 providers resell the Openreach network alone, and around 80 alternative networks (altnets) are tracked by INCA and Point Topic, though four groups still account for roughly 82% of retail connections. Our own directory tracks 429 UK ISPs.

What is an altnet, and how big are they?

An altnet is an alternative network builder outside Openreach and Virgin Media O2. Combined, altnets pass 19.7 million premises with about 3.5 million live connections (INCA, 2026); the largest are CityFibre (4.4m premises), Netomnia/YouFibre (3.4m), nexfibre (2.44m) and Hyperoptic (1.9m).

Is the UK broadband market consolidating?

Yes. nexfibre agreed a £2bn acquisition of Netomnia in February 2026, with the CMA's comment window closed in May 2026 and completion expected later in 2026 subject to clearance; CityFibre has already absorbed Lit Fibre and Connexin. With build costs high, further consolidation is widely expected.

About this report

This report is part of the BroadbandSwitch.uk 2026 Guide Library, published by BroadbandSwitch.uk, the consumer arm of the SearchSwitchSave network. Retail shares are Ofcom's last published official split (2023); current customer bases are company results and Point Topic estimates, clearly labelled as such. Our approach to evidence and corrections is documented in the methodology and trust hub, and every published correction appears in the corrections log.

Take it with you: download the free 6-page PDF report, including all three charts, the market tables and full sources.

Citing this report: BroadbandSwitch.uk. (2026, June 11). UK broadband market share 2026: Who holds the market. SearchSwitchSave. https://broadbandswitch.uk/reports/uk-broadband-market-share/

Sources

- BT Group plc. (2026, May 21). Results for the full year to 31 March 2026. https://newsroom.bt.com/

- Computer Weekly. (2026, March 11). Altnets a force to be reckoned with in UK broadband. https://www.computerweekly.com/news/366639950/Altnets-force-to-be-reckoned-with-in-UK-broadband

- Competition and Markets Authority. (2026). nexfibre / Substantial merger inquiry. https://www.gov.uk/cma-cases/nexfibre-slash-substantial-merger-inquiry

- Independent Networks Co-operative Association. (2026, March 11). State of the altnets 2026. https://inca.coop/state-of-the-altnets-2026/

- Jackson, M. (2026, March). INCA: Alternative full fibre broadband networks cover 19.7 million UK premises. https://www.ispreview.co.uk/index.php/2026/03/inca-alternative-uk-full-fibre-networks-cover-19-7-million-premises.html

- Ofcom. (2025, March 20). Telecoms access review 2026 to 2031: Volume 2, market definition and SMP assessment. https://www.ofcom.org.uk/siteassets/resources/documents/consultations/category-1-10-weeks/consultation-telecoms-access-review-2026-31/

- Ofcom. (2026, March 17). Promoting competition and investment in fibre networks: Telecoms access review 2026 to 2031 (statement). https://www.ofcom.org.uk/phones-and-broadband/telecoms-competition-regulation/

- Ofcom. (2026, April 16). Telecommunications market data update Q4 2025. https://www.ofcom.org.uk/phones-and-broadband/telecoms-research/data-updates/

- Point Topic. (2025). Q3 2025 UK ISP and network supplier metrics: A market overview. https://www.point-topic.com/post/q3-2025-uk-isp-and-network-supplier-metrics-a-market-overview

- Telecompaper. (2026, February 18). Virgin Media O2 loses 18,000 fixed-line, 165,000 mobile connections in Q4. https://www.telecompaper.com/news/virgin-media-o2-loses-18000-fixed-line-165000-mobile-connections-in-q4--1562683

- VodafoneThree. (2025). VodafoneThree begins a new era of connectivity for the UK. https://www.vodafonethree.com/news/new-era-of-connectivity

This report distinguishes throughout between Ofcom's last official retail split (2023), operator-reported figures and commercial estimates; network footprints measure different bases and overlap, so are never summed. Figures are refreshed on results seasons and Ofcom data updates.